By Sheldon Birkett

Preached by business associates, CEO’s, and the wealthy elite, is often stated that an increase in the minimum wage increases long term unemployment, costing the working class. Ontario’s initiative to increase the minimum wage to $15 per hour is a sign that the realities of precarious working conditions, and the adverse effects of globalization are finally starting to be understood by policymakers.

The neoclassical rational expectations model of contemporary economics is still widely believed in as a macroeconomic “law” when it comes to the minimum wage. When people talk about minimum wage increases, individuals fail to consider the fundamental negative relationship between inflation and unemployment: the Phillips Curve. Popularized by Paul Samuelson and Robert Solow as a menu of policy options, the Phillips curve is highly regard as a foundational principal of macroeconomics. Economists such as Edmund Phelps and Milton Friedman, took the idea of the Phillips curve, and used the Phillips curve to further promote the centralized importance of monetary policy and the rational expectations model of macroeconomics. Many say that the direct correlations between inflation and unemployment are not as coherent as one may expect them to be, often characterized as an argument against Freidman’s rational expectations model. Despite the naysayers of the rational expectations model, it can very well be considered that a rational expectations theory can be utilized to justify increases in the minimum wage; implying, a minimum wage increase would hold unemployment constant to the long-run trend with a low sacrifice adjustment ratio.

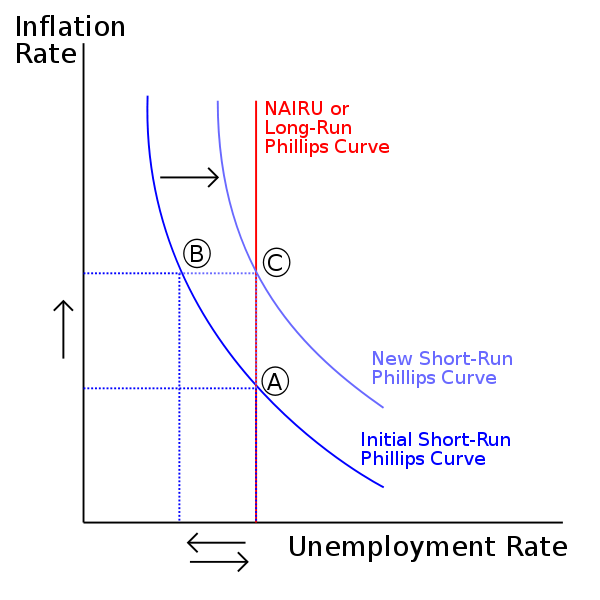

The explicit reasoning of applying a rational expectations model to justify increases in the minimum wage, is due to the neutrality of the unemployment rate around the “natural rate of unemployment.” The “natural rate of unemployment,” is more accurately defined as the “nonaccelerating inflation rate of unemployment,” (NAIRU).[1] The NAIRU is often assumed to be “fixed” or constant in nature, though such an assumption about the macro-economy can be misleading. The NAIRU is determined by real factors affecting the supply and demand for labour, such as demographics, technology, unionization, labour regulation etc. Any variation experienced in the real factors will affect variation in the NAIRU, though the exact deviation of NAIRU variation from the mean NAIRU, is often unknown. The World Economic Forum reported that the difference between British inflation rates and Ireland inflation rates was only 0.05 percent, though the standard deviation between the measures was excess of 2.5 percentage points, which implied (with a 95 percent confidence interval) inflation between Ireland and Britain was 10 percentage points wide.[2] Given the ambiguity in variation of the NAIRU measure, it is difficult to determine the long-term “real” affect an increase in the minimum wage would have on unemployment.

It is true the initial impact of a spike in minimum wage, such as to $15, will increase unemployment; though, it is often overlooked that an increase in the minimum wage will also enhance labour productivity. The mixed results of an immediate minimum wage increase often leads policy officials to reconsider minimum wage increases. If the minimum wage increase is projected on a long-run trend, it is possible to see that an increase in minimum wage will effectively increase inflation, though, the negative externalities inflicted on employment will not persists. At first, the wage increase will increase aggregate demand, increase workers bargaining power, and eventually increase consumer prices, raising the consumer price index (CPI) and inflation. As projected time and time again, there will initially be a decrease in unemployment, advent of experiencing greater aggregate demand. This trend of lower unemployment will eventually return to the natural rate of unemployment (NAIRU) once consumer expectations are adjusted. The time horizon it takes for peoples expectations, to adjust back to the long run trend is debatable. It is certain that an increase in the minimum wage will not increase unemployment in the long run, but in affect, result in lower unemployment rate in the short run. The relational concept of inflation and unemployment rates to increases in the minimum wage is widely misunderstood and overlooked. The importance of the Phillips Curve relationship should not be underestimate in macroeconomics, when considering increases to the minimum wage.

Given the findings about the Phillips Curve, it is apparent that many of the criticisms against a minimum wage increase are inherently embedded in class politics. From a business perspective, it is self-evident that an increase the minimum wage would be cutting away at marginal profits. Individual businesses fail to analyze the return of benefits from a minimum wage increase on the collective economy, and is a classic fallacy of viewing the economy as non-cyclical in nature. Respective on minimum wage increases, it is apparent that precarious labour conditions cannot persists in a globalized economy.

Click Here for a PDF Copy of Ontario Increase in Minimum Wage: A Phillips Curve Analysis

[1] Kevin Hoover, “Phillips Curve,” The Concise Encyclopedia of Economics, 2008, http://www.econlib.org/library/Enc/PhillipsCurve.html.

[2] Stefan Gerlach, “Why the Phillips curve still works for Ireland,” World Economic Forum, July, 22, 2015, https://www.weforum.org/agenda/2015/07/why-the-phillips-curve-still-works-for-ireland/.